Klarna vs. Affirm: Upacking Klarna’s Data and Valuation

A revealing look at merchant networks, revenue models, and valuations in this high-stakes fintech rivalry—leading up to Klarna’s 2025 IPO.

In my last post, I chronicled Klarna’s evolution from a small Swedish startup to a global fintech powerhouse on the cusp of a U.S. IPO. Given Klarna’s upcoming listing, it’s only fitting to size it up against one of its top U.S. competitors—Affirm (AFRM 0.00%↑ ). Both companies are leaders in the Buy Now, Pay Later (BNPL) space, but as I scratched beneath the surface, I found two distinct approaches to generating revenue, managing risk, and ultimately driving value for investors.

In this post, I’ll walk you through the key similarities and differences between Klarna and Affirm, leveraging some insights from my recent X posts. I’ll also touch on how I see Klarna stacking up on valuation compared to its peers. If you enjoy this type of deep-dive analysis, be sure to hit that subscribe button for more updates!

Similar Yet Different: Revenue Mix and Core Strategies

Revenue Breakdown

Klarna: Roughly 84% of Klarna’s revenue comes from transaction and service fees paid by merchants. Interest income still matters—growing at ~20% YoY—but remains a smaller piece of the pie. Klarna’s leadership in transaction-based revenue stands out, bolstered by its extensive merchant network of over 575,000 partners—significantly larger than Affirm’s 303,000 merchants. Both Klarna and Affirm are experiencing strong merchant growth, but Klarna’s head start suggests a network effect that continues to expand.

Affirm: Nearly 50% of Affirm’s revenue stems from lending interest, a fundamentally different approach that relies on customers carrying balances over a longer term. While Affirm also charges retailers fees, it leans more heavily on interest-based lending for growth. As a result, Affirm’s revenue as a percentage of GMV (Gross Merchandise Volume) stands at 9.1%, notably higher than Klarna’s 2.54% take rate. Take rates, as described here, are higher in lending versus payments —but companies like Affirm must continuously refine their ability to manage credit and funding risks effectively since they have a significant risk exposure.

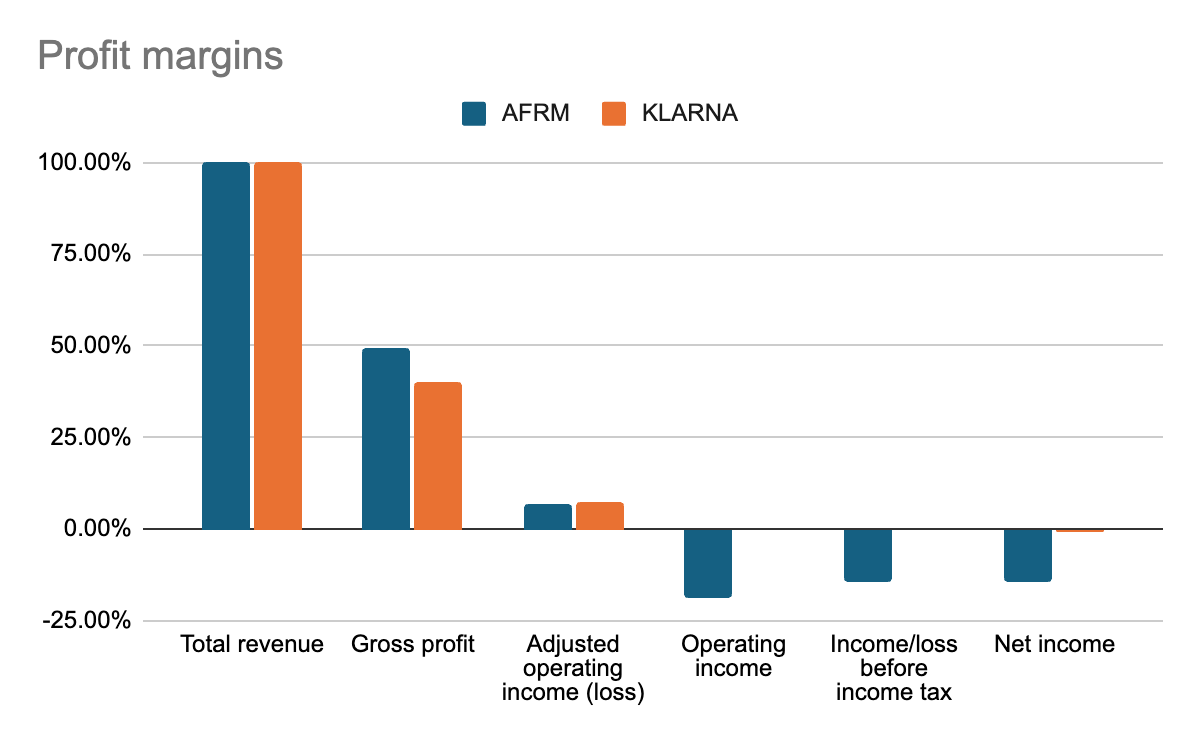

I put together an Income statement adjusted to Klarna’s reporting, since I had more details about Affirm I managed to attribute revenues and costs somewhat accurately. The waterfall chart above shows some of the differences between the two.

Loan Duration and Funding Needs

One of the biggest operational divergences between Klarna and Affirm lies in their lending product, leading to very different average loan durations.

Klarna: Typically 40 days

Affirm: About 11 months

That’s a staggering difference when you think about how quickly each company recycles capital. Klarna’s short cycle means it can turn over its loan book more frequently, requiring comparatively less long-term funding. Affirm, on the other hand, extends credit for longer, which can boost interest income but also elevates liquidity and credit risks.

For investors, these durations have ramifications for growth and profitability. Affirm’s longer-term loans can be lucrative if credit losses remain low, but they also lock up more capital. Klarna’s quicker turnover reduces its total funding requirements and lowers risk exposure—one reason Klarna’s credit losses stabilized at 0.46% in the latest quarter vs Affirms ~1.3%, which is almost 3x more.

Cost Structures and Profit Margins

Klarna has demonstrated a laser focus on operational efficiency. As mentioned in my previous Klarna post, the company reduced operating expenses by 15% in 2023, thanks to strategic layoffs, a pivot toward automation, and AI-driven marketing (which led to almost 3x higher revenue per employee in 2024). These moves contributed to Klarna reporting back-to-back profitable quarters in 2024—a rarity in the BNPL sector and a testament to its leaner cost structure.

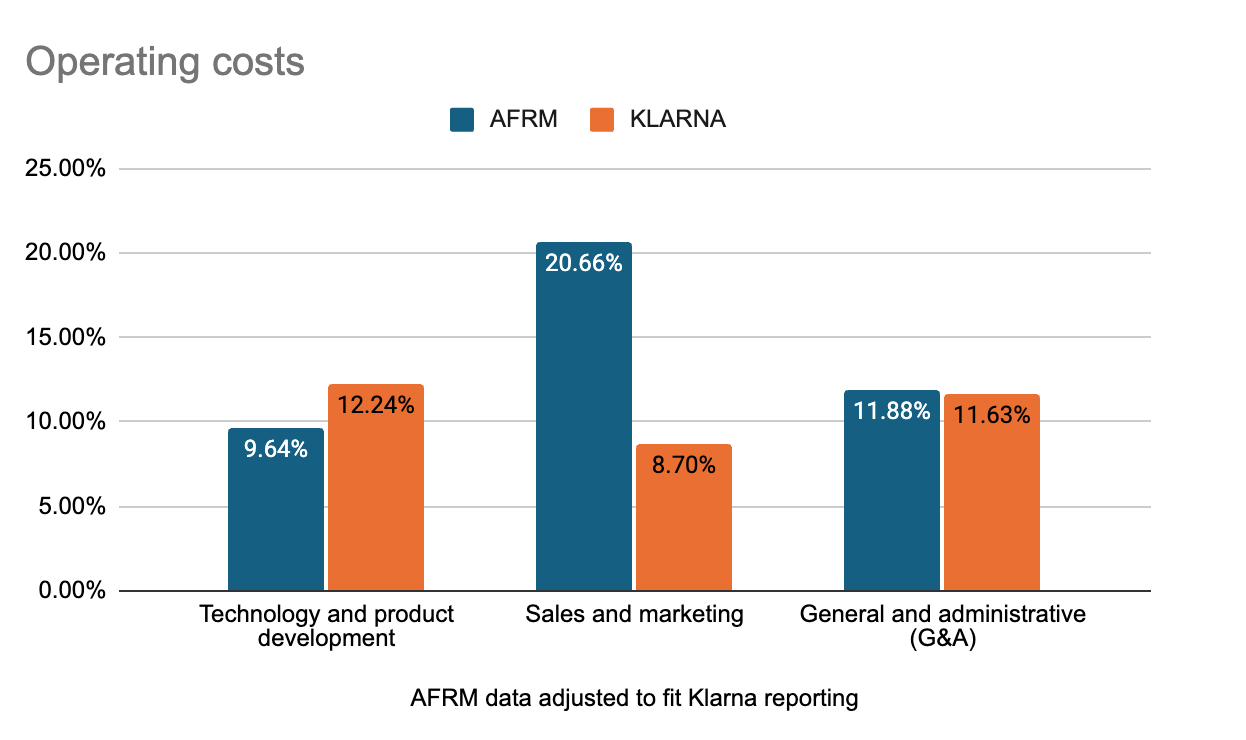

Affirm, meanwhile, benefits from potentially higher margins on extended credit. However, it hasn’t matched Klarna’s success in turning a net profit yet. Its cost of goods sold (COGS) is tied heavily to servicing and funding longer-duration loans instead of processing fees in the case of Klarna. In terms of operating costs, its Sales and Marketing costs stick out (21% vs Klarna’s 9%) indicating a less efficient commercial organization. Affirm also has much higher share-based costs, which is common for US companies, but still affects profitability (I had to extract these from each cost center, S&M, SG&A and R&D). Perhaps they should do like Klarna, and layoff unnecessary sales and marketing staff to lower both of these cost lines.

Valuation: Where Do They Stand?

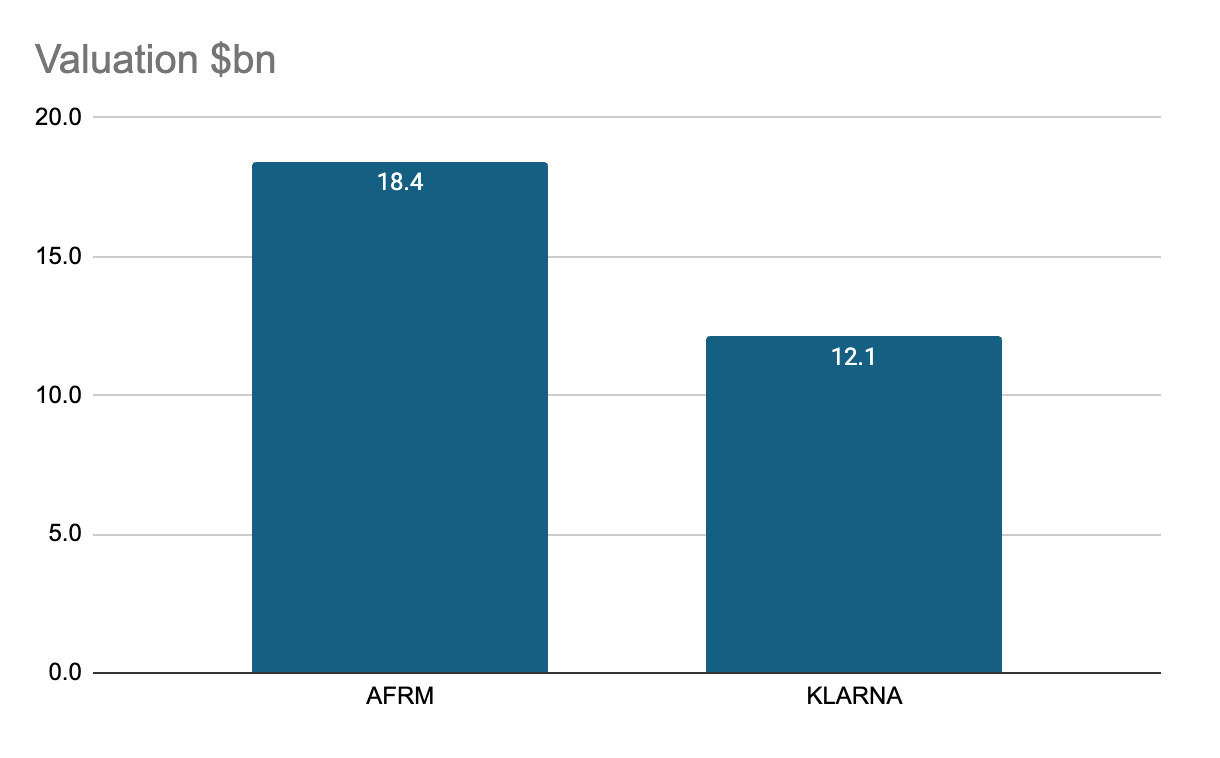

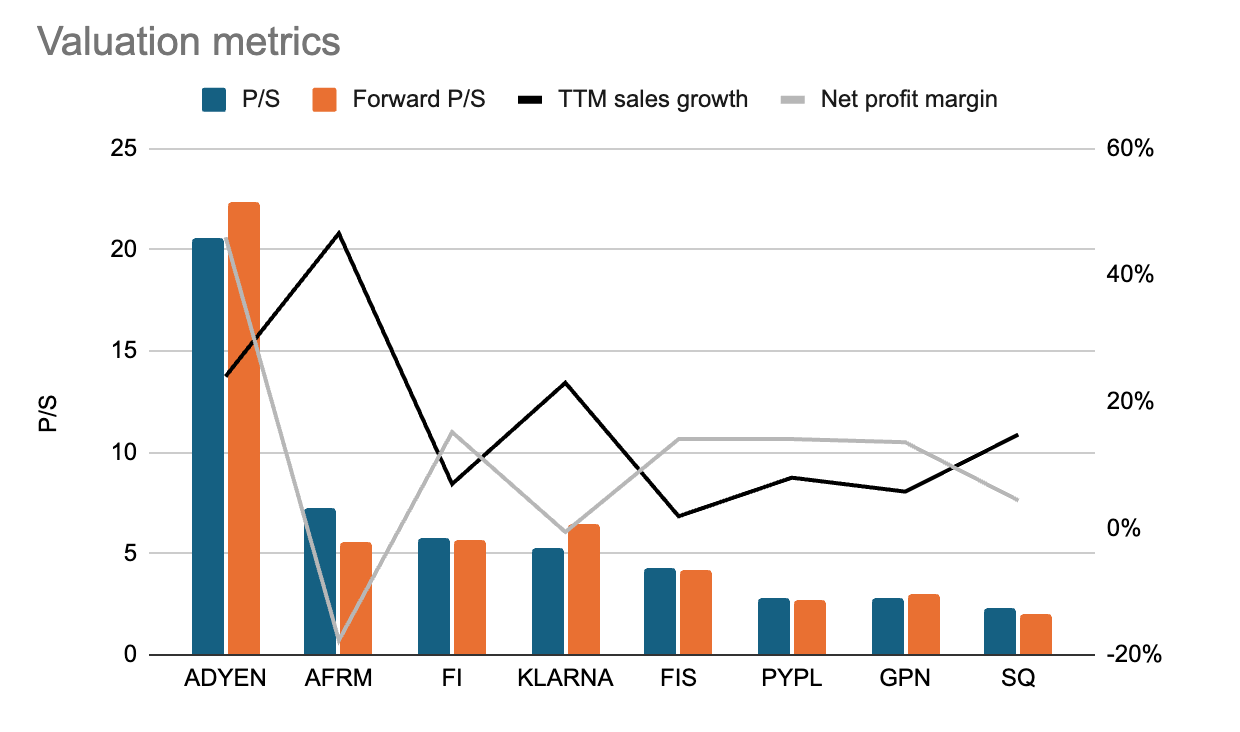

Publicly traded, Affirm’s market cap recently hovered around $19B, giving it a price-to-sales (P/S) ratio of 7.7 (TTM as of Jan ’25). Klarna, on the other hand, was valued at around $12.1B in the OTC (over-the-counter) market as of Nov ’24, implying a P/S ratio of 5.2.

Why the disparity? Well, OTC valuations fluctuate quite a lot. While Klarna’s valuation sat at $12bn in Nov’24, media reports an expected $20bn valuation at its upcoming IPO. Investors may, however, be pricing in Affirm’s revenue-to-GMV ratio of 9.1% and might be a bit less keen on Klarna as another payments company. However, Affirm’s profitability remains elusive. Klarna, nearly net-profitable and highly efficient, trades at a lower multiple, which could represent a value opportunity in the BNPL market, which has been growing, eating into the $1 trillion credit card market.

Klarna’s shorter loan durations and established brand recognition in Europe inspire confidence. Should its U.S. expansion and IPO go smoothly, I wouldn’t be surprised to see a valuation re-rating to closer align with—or even surpass—Affirm’s multiples.

What Comes Next?

Klarna’s U.S. IPO could serve as a litmus test for BNPL valuations. Given rising interest rates and the specter of consumer credit risk, investors are scrutinizing balance sheets more than ever. Klarna’s approach to scaling AI, streamlining marketing, and focusing on a transaction-first revenue model positions it well to weather volatility. Affirm, with its strong partnerships and brand presence in North America, still has significant upside if it can manage credit losses and rein in operational costs. In this area, I believe it needs to step up.

I’ll dig deeper into Klarna, its team, products, valuation, and post-IPO prospects in future posts, so stay tuned. There’s plenty to unpack!

If you’re as fascinated by fintech as I am, be sure to subscribe for more stories like this.